Navigating Uncharted Waters in the Canadian Economy

One of the things that I regularly get involved in is preparing forecasts for clients, usually in specific technology markets. Invariably these forecasts relate in some way to what is happening in the economy at large. In many cases, prospects for the economy drive these forecasts so it is very important for us to have a handle on what is likely to happen in the economy when we prepare our forecasts in various markets. But we have recently entered unknown territory, making forecasting extremely difficult. Let’s start with what we have seen emerging in the economy over the last while.

Canadian economic performance has been fairly good, although by no means stellar, since the recession in 2008/2009 averaging a real GDP growth rate of 2.1% p.a. (CAGR) up to the end of 2019, representing a 10-year period of sustained growth. But storm clouds were brewing as early as March 2019 when the treasury yield curve started to invert.

Inverted Yield Curve

The yield curve is often an indicator that the economy will enter a recession within about 12 to 18 months after the onset of the inversion. The reasons for it being a predictor of a recession are complex and relate to expectations about the economy, about monetary policy and the availability of funds for investment (see this analysis by the Chicago Fed, for example). It has been a remarkable predictor, even though the exact dynamics remain somewhat obscure, yielding only one false positive since 1962.

There are a few caveats.

- A yield curve that inverts for a short period of time is not a good predictor of a recession. It needs to remain inverted for some months before it is regarded as a ‘signal’ worthy of being noted.

- The scale of the inversion is important. A spread of a few basis points is more likely to be noise than signal.

- In those situations where the yield curve is inverted for a month or more, recession could be anywhere between six months and two years away and so it is not an accurate predictor of the timing of the running point.

- In those rare cases where an inverted yield curve does not foreshadow a recession, there is always a softening in economic activity. As many economists and analysts have noted, the yield curve inversion itself is not an economic shock.

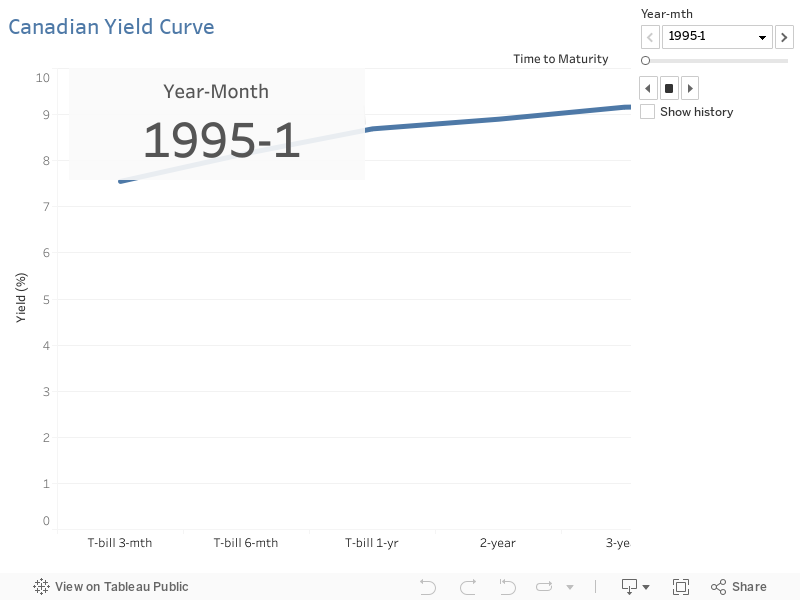

The chart below shows the yields from 3-month Treasury Bills plotted against Government 10-year Bond Yields since 1995. (Note that some analysts look at the spread between the 2-year and 10 bond yields. The predictive power is largely similar.)

The animated visualization that you can access from the link below (which is also embedded at the end of this blog post) shows how yield spreads have changed by month since January 1995 (up until the most recent data up to March 26, 2020).

Looking at the yield curve doesn’t immediately tell you what is going on, although it certainly suggests that something is going on. In the 2008/2009 recession it is unlikely that the inverted yield curve foretold of the subprime collapse, just as the current inverted yield curve could not be a harbinger of the COVID-19 pandemic.

What exactly is going on? There are many things at play. If the inverted yield curve always represents softening of economic conditions, then perhaps it is not surprising that when one or more economic shocks occurs, the economy is driven into recession. This was the case in 1990, when the main economic shocks to the Canadian economy were the US recession, the Bank of Canada’s overreach in trying to quell inflation and Federal tax increases. In 2008/9 it was the financial crisis precipitated by the subprime mortgage fiasco. And in 2020, there is no doubt that the response to the COVID-19 pandemic is an economic shock of note.

Charted Waters

But wait, there’s more, as they say in those infinite Facebook ads. The US-everyone else trade war(s) have had an impact on Canada, with increased duties and increased uncertainty creating an environment of economic instability. Then we had the rail blockades and strikes across the country. The onset of the COVID-19 pandemic and the accompanying contraction in travel has seen an oil price war between Russia and OPEC with prices reaching 18-year lows. This is having a major impact on the Canadian oil patch – as if they didn’t already have enough problems to contend with. And then there’s the massive impact of the pandemic itself. Social distancing, business closures, travel bans, the loss of jobs are all having a devastating effect on the global and Canadian economies. Everything points to us being in for a rough ride.

Watching the different economic forecasts over the past month as they emerge from different sources has been quite revealing, more so of economic psychology (if there is such a thing) than of economics. The forecasts prepared in the first three weeks of March have a decidedly different tone to those from the last week of March. On March 12, Royal Bank was expecting a technical recession in Canada (two consecutive quarters of modest negative growth), but with GDP growing at 0.2.% in real terms over the year. While this does represent a significant drop from the 1.6% real GDP growth experienced in 2019, I think most would agree that if we emerged from the COVID-19 pandemic with that economic result, we could count ourselves as lucky.

At the other end of the spectrum, the Parliamentary Budget Officer noted in the scenario analysis released on March 27 that the COVID-19 pandemic and the oil shocks could result in a decline of 2.5% in GDP in the first quarter of 2020 and a 25% decline in the second quarter (at annual rates) for an overall decline of 5.1% over the year. Unemployment in the third quarter would reach a record 15%. Granted, they make the point very strongly that this is one of many scenarios that they are considering and that this is not a forecast, but it is telling that this is the only scenario published in response to COVID-19 so far.

The impact on the economy is also dependent on how the government reacts, specifically in terms of measures to stimulate the economy or keep businesses afloat. The logic of stimulus is fairly simple. If the Canadian economy is likely to ‘lose’ $200 billion in GDP through reductions in consumer spending, investment and other non-governmental components of GDP, by injecting $200 billion of government funds into the economy we should break even. The Canadian Government’s stimulus package is currently in the region of $200 billion. We are almost as low as we can go in terms of interest rates so there is not much more that we can do in terms of making money cheaper for borrowers. It is unlikely that we have seen the end of the stimulus measures.

Into the Unknown

With the COVID-19 pandemic situation changing daily and the responses of consumers, businesses and governments still far from settled, how do we navigate into the unknown when fathoming the unknown is important for our business? There is still much uncertainty about how to tackle the COVID-19 situation, with some experts saying that we can start seeing the new normal after another month, while others are looking at lockdowns until August.

Scenario analysis is an extremely effective approach for defining the cone of uncertainty around where the economy is headed. Typically, this would involve creating a worst-case scenario, a best-case scenario and a most likely scenario. But it only tells us the consequences of the risks that lie ahead. It is not a guide for action.

McKinsey has recently published a thought piece on the ‘Implications of COVID-19 for Business’. They recommend that companies think and act across five horizons, each one further afield from the previous one and ranging from addressing immediate business challenges to thinking through how the industry may shift in the post-pandemic era.

The fact is that there are no easy solutions or magic crystal balls that give anyone a clear view of the future. Much like the navigators of old who faced the prospect of dragons when they sailed into the unknown, the horizon shrinks to what we can discern through the fog at close quarters. Our immediate challenge is not to run aground and we also know that if we see land, we will recognize it. And hopefully we don’t encounter those dragons.